5 Critical Mistakes People Make After a Car Accident (That Hurt Their Case)

These common errors can cost you tens of thousands in compensation—here's what personal injury attorneys see victims do wrong, over and over again.

Every personal injury attorney has seen it countless times: a client walks in with a legitimate accident case, clear injuries, and obvious liability—but they've already destroyed their own claim without realizing it. A single conversation with an insurance adjuster, a gap in medical treatment, or a casual social media post can turn a six-figure settlement into nothing.

The harsh reality is that insurance companies are banking on you making mistakes. They've studied accident victims for decades and know exactly which errors people make in the vulnerable, chaotic hours and days after a crash. Their adjusters are trained to exploit these mistakes to minimize or deny your claim entirely.

Below are the five most damaging mistakes we see accident victims make—and more importantly, what you should do instead to protect your legal rights and maximize your compensation.

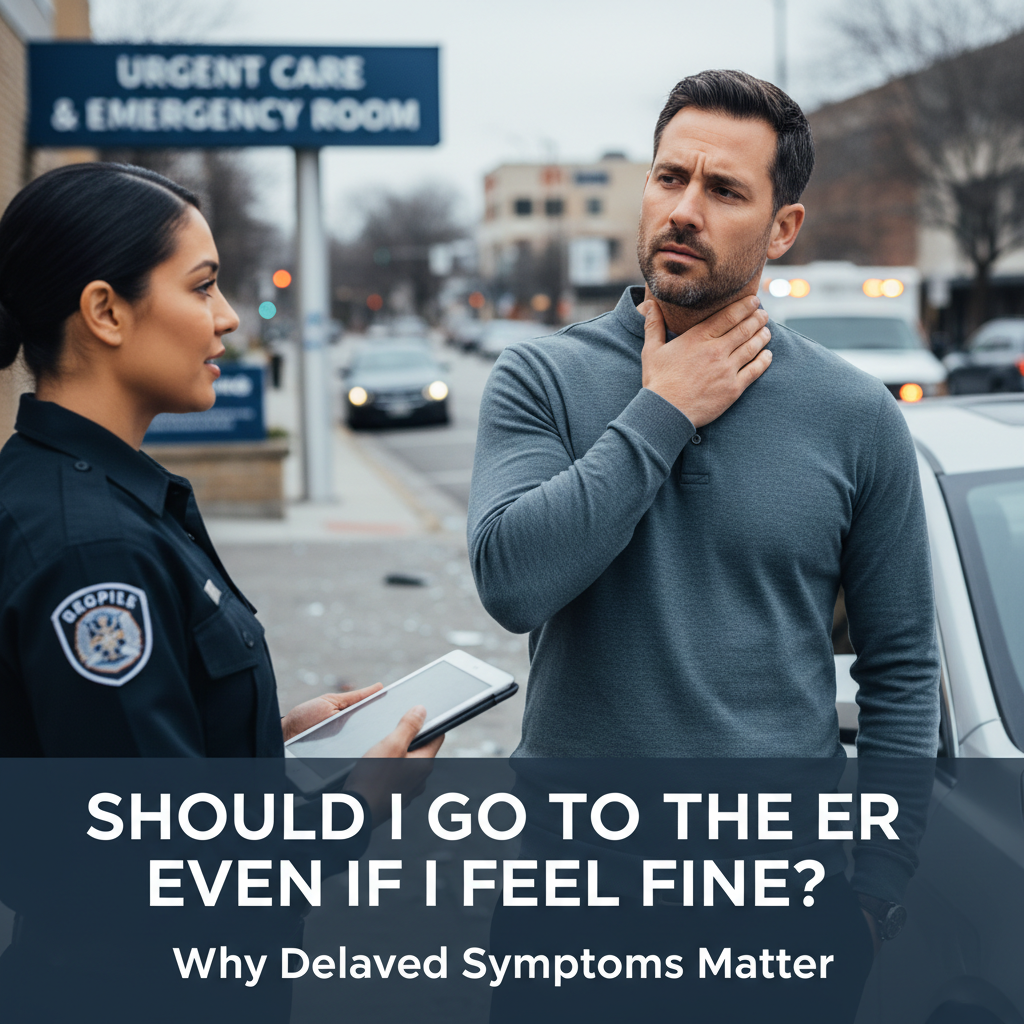

Delaying or Skipping Medical Treatment

This is the single most damaging mistake accident victims make, and it happens constantly. You feel shaken up but "okay" at the scene. The adrenaline is pumping. You decline the ambulance. You go home, take some ibuprofen, and figure you'll see how you feel tomorrow.

Two days later, your neck is killing you. Your back has stiffened up. You're getting headaches. Now you go to urgent care—but from a legal standpoint, significant damage has already been done.

Why This Destroys Your Case

Financial Impact

Insurance companies will argue that if you didn't seek immediate medical care, you couldn't have been seriously injured. They'll claim your injuries developed later from something else—not the accident. This defense works remarkably well with juries who don't understand that many serious injuries (whiplash, concussions, soft tissue damage, internal injuries) don't manifest symptoms immediately.

The insurance adjuster's playbook literally includes talking points like:

- "If they were really hurt, they would have gone to the hospital right away."

- "The gap in treatment shows the injuries weren't caused by our insured."

- "They were fine for three days—this is clearly a different injury."

Medical professionals call this the "seat belt sign phenomenon"—injuries that are absolutely real but don't hurt until hours or days later when inflammation, muscle spasms, and swelling set in. Insurance companies call it "an excuse."

Do This Instead

Seek medical evaluation within 24 hours, even if you feel fine. Go to the ER if the ambulance offers transport. If you decline transport, visit an urgent care or your primary care physician the same day or next morning. Tell them you were in a car accident and want to be checked for injuries. Document everything. This creates an unbroken chain of medical evidence from the accident to your treatment.

"I've seen cases where a client waited just 48 hours to see a doctor and it cost them $40,000 in settlement value. The insurance company argued they weren't hurt at the scene and their later symptoms were unrelated. We couldn't overcome that gap."

Giving a Recorded Statement to the Other Driver's Insurance

The other driver's insurance company will call you within hours of the accident—sometimes before you've even seen a doctor. The adjuster will be friendly, sympathetic, and seem genuinely concerned about your wellbeing. They'll say they "just need to get your version of what happened" and ask if they can record the conversation "for quality assurance purposes."

This is a trap.

Insurance adjusters are trained in interrogation techniques. They know how to ask leading questions, get you to minimize your injuries, accept partial fault, and contradict yourself—all while sounding like they're on your side.

Questions They'll Ask (And Why They're Dangerous)

- "How are you feeling right now?" If you say "I'm okay" or "I'm fine," they'll use that against you later when you claim injuries.

- "Were you wearing your seatbelt?" If you hesitate or aren't 100% certain, they'll argue you contributed to your injuries.

- "How fast were you going?" Any estimate you give can be used to argue you were speeding or driving recklessly.

- "Did you see the other car before the impact?" They're looking for ways to argue you could have avoided the accident.

- "Have you ever been in an accident before?" They want to find pre-existing injuries to blame instead of this accident.

Financial Impact

A single recorded statement made in the first 24 hours—when you're in pain, medicated, and not thinking clearly—can reduce your settlement by 40-60%. Attorneys regularly see cases where clients said something innocuous that the insurance company later twisted into a complete defense.

Do This Instead

Politely decline to give a recorded statement. You are NOT legally required to talk to the other driver's insurance company. Say: "I'm still receiving medical treatment and gathering information about the accident. I'm not comfortable giving a recorded statement at this time. Here's my contact information, and I'll have my attorney reach out to you." Then consult with a personal injury attorney before saying anything else.

You DO need to report the accident to your own insurance company (it's in your policy), but even with your own insurer, keep initial statements brief and factual. Save detailed discussions for after you've consulted with an attorney.

Accepting the First Settlement Offer

The insurance company makes you a quick offer: $5,000 to "make this easy" and "cover your expenses." You have $2,000 in medical bills so far, and $5,000 sounds like free money. You sign the release.

Three weeks later, your doctor says you need an MRI. It reveals a herniated disc requiring months of physical therapy and possibly surgery. Your medical bills balloon to $45,000. You can't work for two months—that's $12,000 in lost wages. And now you're stuck, because you already signed away your rights for $5,000.

Why Initial Offers Are Always Lowball

Insurance companies make quick settlement offers for two strategic reasons:

- You don't know the full extent of your injuries yet. Many serious conditions (herniated discs, traumatic brain injuries, internal organ damage, psychological trauma) take weeks or months to fully diagnose.

- You're financially vulnerable. They know you're stressed about medical bills and lost income. A quick $5,000 looks appealing when you're worried about paying rent.

Once you sign that release, you cannot go back for more money later—even if you discover injuries you didn't know about.

Financial Impact

Initial settlement offers are typically 10-20% of what the case is actually worth. Attorneys routinely negotiate settlements that are 5-10x higher than the insurance company's first offer. In one study, the average settlement with attorney representation was $77,600 versus $17,600 for those who accepted initial offers without legal help.

Do This Instead

Never accept the first offer—or any offer—without consulting an attorney. Most personal injury lawyers offer free case reviews. They can tell you what your case is actually worth based on your injuries, lost wages, and state laws. Even if you ultimately settle without hiring an attorney, at least you'll know what you're leaving on the table.

⏰ Time Pressure Is a Tactic

If an adjuster says "this offer expires in 48 hours" or "we need an answer today," that's a pressure tactic. Legitimate settlement negotiations don't have arbitrary deadlines. They're trying to prevent you from consulting with an attorney who would tell you the offer is garbage.

Posting About the Accident on Social Media

You post on Facebook: "Thank God I'm okay! Scary accident this morning but I walked away with just some bumps and bruises 🙏"

Or you're on Instagram two days later at your niece's birthday party, smiling in photos, playing with the kids.

Or you tweet: "Some idiot ran a red light and totaled my car. Unbelievable."

Every single one of these posts can—and will—be used against you in your injury claim.

How Insurance Companies Use Social Media

Insurance adjusters routinely monitor accident victims' social media profiles. They have investigators who screenshot every post, photo, and comment. They're looking for:

- Minimization of injuries: If you said you're "okay" or just have "bumps and bruises," they'll argue you weren't seriously hurt.

- Physical activity: Photos of you standing, lifting things, playing sports, or even just smiling are used to argue you're not in pain.

- Admissions of fault: Any statement about what happened can be used to show you were at fault or distracted.

- Contradiction with medical claims: If you claim you can't work or do normal activities, but your Instagram shows you at concerts or hiking, your credibility is destroyed.

Financial Impact

A single Facebook post saying "I'm fine!" has been used to reduce settlements by $50,000+. Photos showing you doing activities you claimed you couldn't do can result in complete claim denial. Insurance defense attorneys will blow up your social media posts into poster-size exhibits for the jury.

Do This Instead

Do not post anything about the accident on social media. Period. Don't discuss it, don't share updates, don't post photos until your case is completely resolved. Set all your profiles to private (though that won't stop investigators from getting screenshots from your "friends"). Better yet, take a complete social media break during your case. Tell your friends and family not to tag you in photos or posts.

"I had a client with a legitimate back injury lose her entire case because she posted photos from a wedding where she was standing and dancing. Never mind that she was in excruciating pain and on medication—the jury saw the photos and didn't believe anything else she said."

Not Documenting Everything

You're hurt, overwhelmed, and dealing with medical appointments, insurance calls, and trying to get your car fixed. Documentation feels like paperwork you'll get to "later."

But six months down the road when you're in settlement negotiations, you have no photos of the accident scene, no journal of your daily pain, no receipts for parking at medical appointments, no record of the days you couldn't work, and no written notes from conversations with the insurance adjuster.

You're trying to reconstruct everything from memory—and the insurance company knows it.

What Gets Lost Without Documentation

- Pain and suffering: Without a daily journal, you can't prove the ongoing impact of injuries on your life.

- Out-of-pocket expenses: Parking fees, prescription costs, medical equipment, home health care—it all adds up, but only if you document it.

- Lost income: You need to prove missed work days, lost overtime, and career impacts.

- Scene evidence: Weather conditions, road hazards, visibility issues all fade from memory.

- Witness information: That person who saw everything? You forgot to get their name, and now they're gone forever.

Financial Impact

Poor documentation can reduce your settlement by 30-50%. Items you can't prove with documentation simply don't get compensated. That's thousands of dollars in legitimate expenses that you eat because you don't have receipts or records.

Do This Instead

Create a comprehensive accident file from day one. Include:

• Photos and video of accident scene, all vehicle damage, injuries

• Daily pain journal (pain levels 1-10, activities you couldn't do, sleep quality)

• All medical records, bills, and receipts

• Lost wage documentation (paystubs, employer letters, tax returns)

• Every out-of-pocket expense with receipts

• Written notes from every insurance conversation (date, time, who you spoke with, what was discussed)

• Witness contact information

• Police report (get a copy within a week)

Use your smartphone to take photos of everything. Create a dedicated folder in your email for all accident-related correspondence. Keep a notebook by your bed to journal before you forget daily symptoms.

The Common Thread: Acting Without Legal Guidance

Notice what all five of these mistakes have in common? They happen when accident victims try to handle everything themselves without understanding the legal implications of their actions.

Insurance companies know this. They're counting on it. They know you're vulnerable, stressed, in pain, and unfamiliar with personal injury law. They know you'll say the wrong thing, accept a lowball offer, or fail to document crucial evidence.

That's why the single most important thing you can do after an accident is consult with a personal injury attorney before making any decisions. Most offer free case reviews with no obligation. They can tell you:

- What your case is worth based on your specific injuries and circumstances

- What to say (and not say) to insurance adjusters

- What evidence you need to gather and preserve

- Whether settlement offers are reasonable or insulting

- How to avoid common pitfalls that destroy cases

And here's the key: most personal injury attorneys work on contingency, meaning you pay nothing upfront and they only get paid if you win. There's literally no financial risk to getting professional legal advice.

🎯 Bottom Line

The five mistakes that destroy car accident cases are: (1) delaying medical care, (2) giving recorded statements to insurance adjusters, (3) accepting the first settlement offer, (4) posting on social media, and (5) failing to document everything. All five can be avoided with proper legal guidance in the critical first days after your accident.

What to Do If You've Already Made These Mistakes

If you're reading this and thinking "I already did some of these things," don't panic. Experienced personal injury attorneys have salvaged cases with far worse fact patterns.

A good lawyer can:

- Explain gaps in medical treatment with expert medical testimony

- Use medical evidence to show injuries were present even if you said you were "fine"

- Contextualize social media posts to show they don't tell the full story

- Reconstruct missing documentation through other evidence sources

- Negotiate with insurance companies who are using your mistakes against you

The key is to stop making MORE mistakes. Get legal representation now, be completely honest with your attorney about what you've said and done, and let them develop a strategy to overcome the damage.

Your case isn't necessarily dead—but every day you wait without proper legal guidance is another opportunity to make it worse.